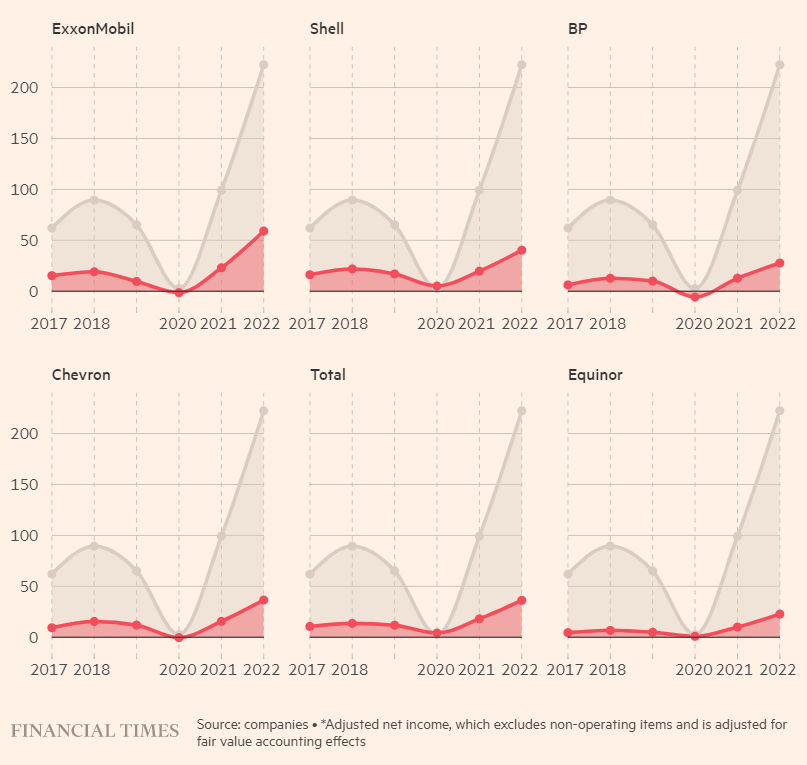

In 2022, the six largest western oil companies made more money than in any year in the history of the industry: over $200bn, largely from pumping and selling the fossil fuels the world must replace to avert the climate crisis.

The windfalls that BP, Chevron, Equinor, ExxonMobil, Shell and Total revealed in their end-of-year results have sparked outrage and accusations of war profiteering. It has also cast doubt over the commitment of executives, politicians and investors to the Paris climate agreement to slow global warming by bringing down emissions.

After years of pressuring Big Oil to curb production, political leaders from London to Berlin to Washington changed tack last year as prices surged, calling on companies to boost output or help them procure replacements for Russian fossil fuels following Moscow’s full-scale invasion of Ukraine.

Those companies that were best positioned to respond were the most rewarded by investors. US giant ExxonMobil, which has resisted pressure to decarbonise more than any other energy major, increased production in 2022 and its shares rallied more than 50 per cent in the year as it raked in a record $55.7bn in profits.

A sizeable surfeit for the supermajors

Oil majors profits ($bn)*

This week BP, the oil major that had gone the furthest in its commitments to the energy transition, announced that it would slow the pace it reduces oil and gas output this decade, meaning its emissions would also decline more slowly.

The U-turn dominated headlines, stirring anger from environmentalists and adding more fuel to calls for windfall taxes. Yet the market approved — BP’s shares rallied more than 10 per cent over the following 48 hours, reaching their highest level in three-and-a-half years.

Western policymakers are still committed to the energy transition. The EU has accelerated plans to rollout renewable power and hydrogen projects across the bloc as a way to replace dependence on Russian fossil fuels. Across the Atlantic, Joe Biden’s Inflation Reduction Act promises to supercharge green investments.

But resurgent demand for hydrocarbons, the blockbuster profits reaped by those who deliver them and the response from the markets have raised serious doubts over whether legacy industries and their investors will ever drive decarbonisation.

“There has really only ever been one way to get the world off oil and gas and that is not to expect the companies who benefit most from that industry to lead the way,” says Adrienne Buller, research director at Common Wealth, a UK think-tank. “These companies are set up to maximise returns to their shareholders and they’re doing exactly that.”

Beyond petroleum?

When BP chief executive Bernard Looney launched his plan to overhaul the British energy company in 2020, the environmental, social, and governance (ESG) movement was in the ascendancy, dominating conversations among European asset managers and on Wall Street.

In response, the newly appointed Irish executive pledged to bring down the company’s carbon emissions by cutting the group’s oil and gas production by 40 per cent and acquiring 50GW of renewable power, all by 2030.

The plan was by far the most ambitious in the sector — still no other oil and gas major has a hard target to cut production — and it looked visionary as crude prices collapsed during the lockdowns of the coronavirus pandemic.

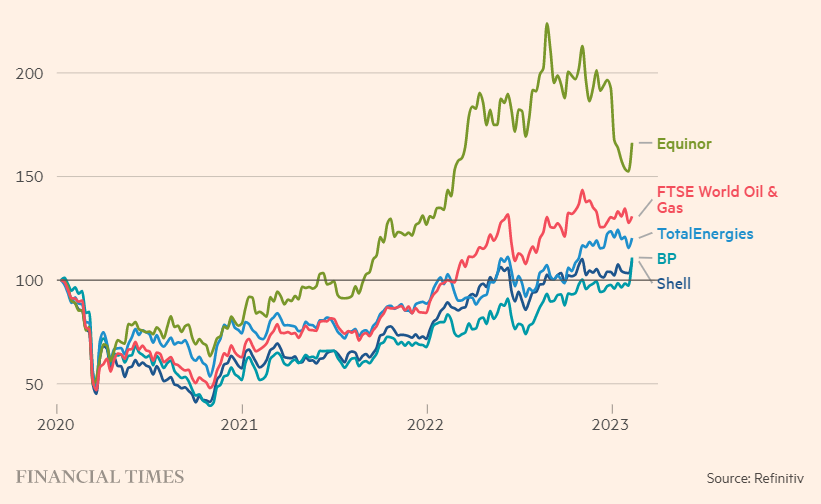

Yet to Looney’s dismay, investors did not reward his efforts. Despite rallying strongly last year, BP’s share price performance has typically lagged its rivals ever since his appointment.

BP’s share price has mostly trailed rivals under Looney

Share prices and index rebased in sterling terms

BP has now rowed back part of that plan. The group’s oil and gas output will now decline by only 25 per cent by 2030, compared with 2019 levels, so its emissions will also fall more slowly. “Governments and societies around the world are asking companies like ours to invest in today’s energy system,” Looney told the FT on Tuesday after reporting a record $27.7bn in profits.

The announcement made waves across the industry. Some saw it as a welcome concession to reality. It was a signal that energy security “has been invited to the energy transition table”, says Jeff Ubben, a US hedge fund activist investor and Exxon board member. “The dinner conversation now includes affordability and reliability, which makes it more robust,” he adds.

It is the second time BP has reversed on a plan to move away from oil in favour of clean energy production. The first attempt, under chief executive Lord John Browne’s “Beyond Petroleum” strategy in the early 2000s, was abandoned a few years later as crude prices soared towards their historic peak in 2008 of almost $150 a barrel.

Looney frames this latest shift not as a change of strategy, but a strengthening of it. At the same time as investing an additional $8bn in oil and gas between now and 2030, the group will also spend $8bn more on its “transition” businesses, he said — biofuels, convenience, charging, renewables and hydrogen.

The adjustment by BP need not be seen as the death knell for Big Oil’s effort — at least in Europe — to become Big Energy, says Nick Stansbury, head of climate solutions at Legal & General Investment Management, a BP shareholder. “I definitely don’t think that what we’re seeing at BP tells you that it’s the wrong thing for a big oil company to try to transition its business model in the right way to make it fit for the future.”

The challenge for chief executives, Stansbury says, is how to transition while protecting financial performance during what promises to be an era of extreme commodity price volatility, as the world’s energy system moves from fossil fuels to renewable power.

“We want these businesses to develop in such a way that they are resilient and poised for success in a net zero world,” Stansbury adds. “Investors are not yet confident of that today, in part because of the lack of certainty and clarity that exists around what the energy system of the future is going to look like.”

That market tension can be seen in the reluctance among executives at the energy majors to bet bigger on uncertain future revenues from renewables, analysts say.

Shell, Europe’s biggest energy company, doubled its profits in 2022 to almost $40bn — the highest in its 115-year history — but left its capital spending plans unchanged. Shell spent $3.5bn on its renewables and energy solutions division in 2022, representing only 14 per cent of the group’s total capital spending. It will spend about the same in 2023.

“Oil companies will complain that they didn’t get any reward in the market for being greener than Exxon,” says Rachel Kyte, dean of Tufts University’s Fletcher School and a former UN climate adviser. “I don’t think that’s enough of an excuse, but I do think it asks a fundamental question of the strategies around the energy transition: how do we send signals in the market that show that we value this kind of oil and gas company better than another one?”

Oil runs the world

In the US, oil executives are doing even less to build out alternative low-carbon businesses and feel they have been vindicated by the meteoric rise of their share prices in the past 12 months. Shale producers dominated the list of best performers on the S&P 500 last year.

“The reality is, [fossil fuel] is what runs the world today,” Chevron chief executive Mike Wirth, told the FT in a recent interview at its headquarters in San Ramon, California. “It’s going to run the world tomorrow and five years from now, 10 years from now, 20 years from now.”

The company made $35.5bn in profits last year and announced plans to return a gargantuan $75bn to investors through share buybacks. In contrast it will spend only $2bn on low-carbon projects in 2023 out of a total capex budget of $14bn, and $10bn between now and 2028.

Investors point to the fact that oil and gas has always been a cyclical industry, where companies boost returns to shareholders during periods of high prices to make up for long periods of underperformance when prices are low. In addition, executives cannot simply “rip up” years of corporate strategy by ramping up capital spending after profits rise, one investor adds.

On Wall Street, there has been a palpable shift back in favour of western oil and gas producers, say people familiar with the pitches made by supermajors to their investors in recent months. Some position it as a question of energy security. In the wake of the Russian energy war with Europe, holding back funding for US producers would be the “road to hell for America”, JPMorgan’s chief executive Jamie Dimon told Congress last year.

However, the record $110bn in dividends and share repurchases paid out to investors in 2022 by the western majors has provoked outrage on both sides of the Atlantic at a time when households are struggling with soaring bills and the low-carbon energy system is crying out for more investment.

Reporting such profits “in the midst of a global energy crisis” was “outrageous”, US president Joe Biden said in his State of the Union address to Congress this week. He also proposed quadrupling tax on corporate stock buybacks.

But Biden has also sent mixed signals about the energy transition. Despite signing into law a $369bn package of clean energy subsidies and once promising to “transition from oil”, Biden spent much of the past year calling for shale oil and gas producers to ramp up supply and released millions of barrels of crude from the US strategic reserve in an effort to drive down fossil fuel prices.

Some believe Big Oil should mostly leave the energy transition up to others. Charlie Penner, a former executive at US hedge fund Engine No. 1 who led and won a 2021 activist campaign at Exxon to take decarbonisation more seriously, says that as long as oil majors are avoiding long-term, low-return projects they should be encouraged to return cash to their investors.

“Without better alternatives, that capital can and should be returned to shareholders who can diversify, including investing in the energy transition, themselves,” he says. Indeed, he and other climate-focused Exxon investors do not think investment in lower-return renewable projects is a sensible use of capital.

BP, for now, is still trying to do both. Over the next eight years, Looney has committed to invest $60bn in BP’s energy transition businesses, which will represent over 50 per cent of its spending in 2030. “I take this as a sign of support and trust in the strategy and the capability that we have been building,” says Anja-Isabel Dotzenrath, BP’s executive vice-president in charge of hydrogen and renewable power projects, which represent about half of that “green” budget.

Rather than slow progress, Dotzenrath argues a new global focus on energy security due to the impacts of the war in Ukraine can accelerate the energy transition by encouraging more investment in domestic renewables as an alternative to imported fossil fuels.

However, even with the impetus of renewables-driven energy security, BP may need more help from policymakers and regulators to convince investors to stick with it through the transition.

“We are relying on a hodgepodge of voluntary codes, voluntary standards, and the markets,” says Kyte at Tufts. “Regulation and legislation for the transition and net zero is woefully missing in action.”

Extracted from Financial Times