Viva Energy has further lowered expectations for earnings this June half, but has encouraged investors with news of a rise in volumes of petrol and diesel sold and a stabilisation of the decline at the retail alliance with Coles.

Viva chief executive Scott Wyatt pointed to weak retailing margins, tough competition in the commercial sector and only a slim profit at the Geelong refinery in Victoria in updating investors on the outlook for first half profit.

But the difficulties in the fuel supply market have been well flagged, including by rival Caltex last week, and investors appear to have taken heart from news that Viva expects a 2 per cent gain in sales volumes this half and an end to the slide in sales at the retail alliance with Coles.

The rise in Viva’s volumes comes against a broader flat market in diesel and jetfuel demand in Australia in the first four months of the year compared to a year earlier, and a 3-4 per cent drop in petrol demand, according to official figures.

“It seems to me that Viva is doing very well in the market in terms of volume,” Merrill Lynch analyst David Errington said on a Caltex conference call with investors.

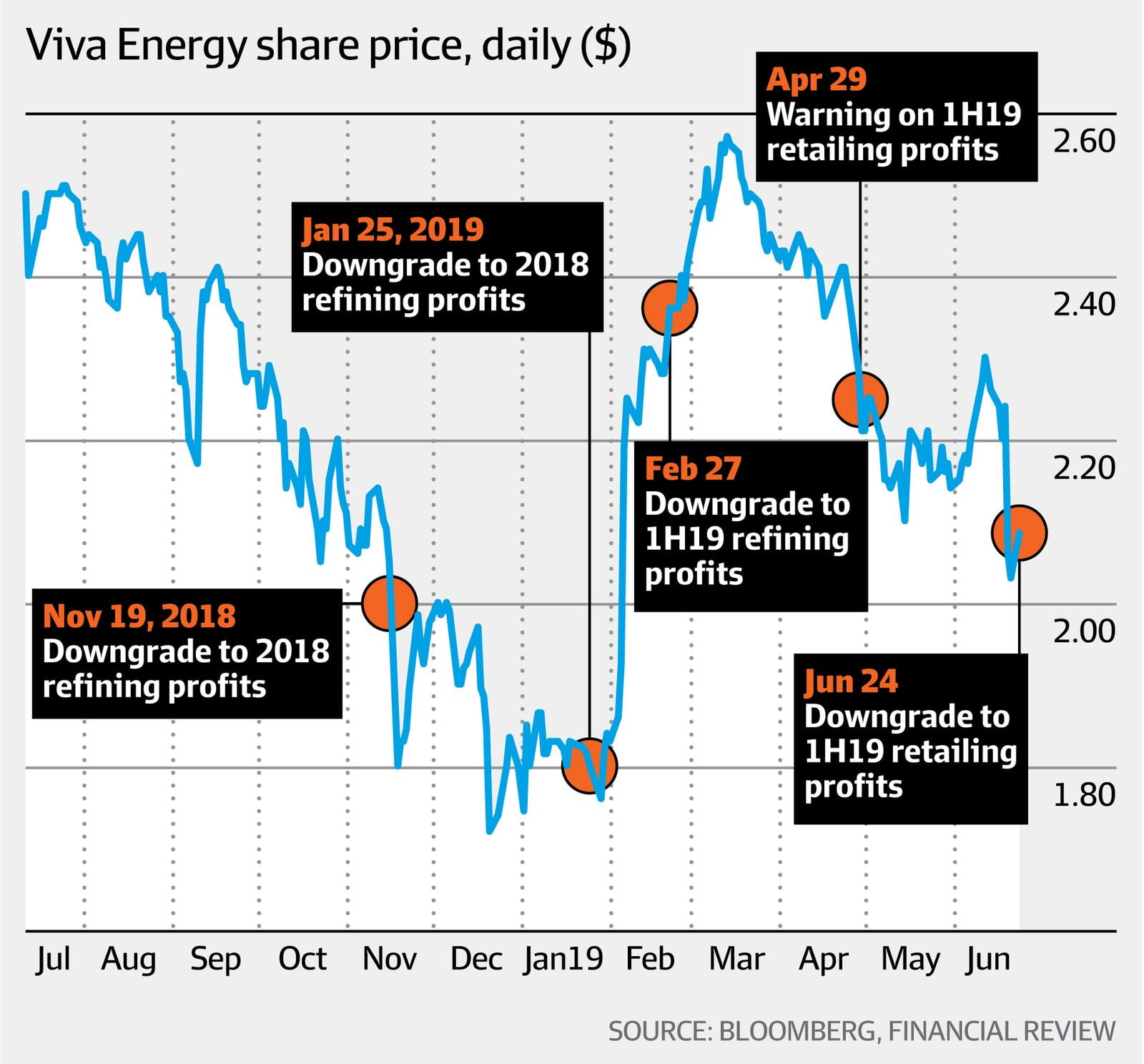

Shares in Viva recovered from a modest loss in early trading to close 4.4 per cent higher at $2.12 on Monday. They lost 8 per cent last Thursday when Caltex issued its profit warning, alerting investors to the weak conditions in both refining and retailing.

Underlying net profit for the first half is expected to be about $60 million-$80 million, Viva said on Monday, adding that underlying earnings in refining would be between zero and $20 million due to weak refining margins.

Group-wide earnings before interest, tax, depreciation and amortisation for the June half would be $150 million-$180 million, Viva advised.

Shares in Viva were sold in the company’s $2.65 billion initial public offer last July at $2.50 apiece. Since then the company has lowered estimates for earnings in either refining or retailing four times, before Monday’s announcement, mostly due to external factors beyond its control.

Speaking to investors in a conference call, Mr Wyatt described the first half as “challenging”. He said refining margins had weakened again after an improvement in April and voiced little optimism of any improvement in the short term.

But he was upbeat about the performance in the revamped alliance with Coles, where Viva has taken back responsibility for pump pricing, promising to restore competitiveness in pricing at the service stations.

“The most important thing for us was to arrest the decline and I am pleased that we have stabilised the business now and have a much more solid platform to begin to re-grow,” Mr Wyatt said. He added that Viva is investing in marketing campaigns to re-engage with customers and restore perceptiveness of the Coles alliance as a competitive fuel supplier.

Sales volumes under the Coles alliance are still lower this half than a year ago, but growth in volumes with existing customers both in the retail space outside the alliance and in the commercial market drove the modest increase in overall volumes.

Underlying EBITDA for the retail business this half is expected to be between $275 million and $290 million, lower than guidance in April of $286.9 million-$291.9 million.

The retailing result would be about 8 per cent down on the $308 million recorded in the first half of 2018. Mr Wyatt pointed to several forces at play, including the rising oil price, which compressed volumes and margins, and adjustments in the competitive retailing market as rivals made changes in response to the revamped Coles alliance and as Woolworths service stations passed into the ownership of Euro Garage.

In the commercial business, underlying EBITDA is expected to be $150 million-$160 million, compared with previous guidance of $164.5 million, Viva said.

“Competitive pressures and higher than expected supply chain costs in some segments have impacted these results,” Viva said of the commercial division.

“The company will focus on improving margin performance through cost and supply chain efficiencies together with minimising exposure to low margin business.”

In refining, Viva said soft regional demand was weighing heavily on margins despite “some modest improvement” in March and April. But the company said it was pleased with “strong” production performance at the Geelong plant this half, with 17.8 million barrels of crude oil processed in the first five months of 2019 and 21 million barrels expected for the full first half.

Mr Wyatt said Viva was “optimising” production at Geelong to make the most of stronger diesel margins, with record diesel production in March and April.

Extracted from AFR